Ništa ne raste pravocrtno kolega BudFox... Korekcija je zdrava i idemo dalje......

DRY BULK

-

-

-

Ajde nam kolega Jasko pojasni, zašto se na Braemer Screen-u onda sve crveni danas?

Jucer niste kolega to pitali kad je bilo zeleno primjetit cu

Napisao sam bio da se prate indeksi, a kada je Braemar otišao u zeleno porasla je cijena ATPL.

Kolege, vidim da me ismijavate na ovoj temi, pa se zabavljajte dalje bez mene

.

.Želim vam svima sreću i da ATPL dođe na 1000 kn, što je bio i moj san.

Nedostatak kritičkog mišljenja nije plus, kako neki ovdje smatraju, nego minus,

ali Idem se ja dalje baviti turistima.

P.S. JFTR, kolegu maratonca sam bio prije 2 godine upozorio na privat da će Dalekovod u stečaj,

kada je cijena dionice bila na 8 kn, jer sam bio dobio infomacije iz prve ruke, pa neka kaže da

to nije istina, a sada ovako prema meni.

-

Zna netko zašto Joakim predviđa toliko niže vozarine za Handye, a sada su al pari s ostalima?

-

Zna li se od cega ce se raditi ovi novi brodovi, jel izmisljen neki novi materijal s obzirom da svi narucuju u Kini a problemi sa celikom.

-

Zna li se od cega ce se raditi ovi novi brodovi, jel izmisljen neki novi materijal s obzirom da svi narucuju u Kini a problemi sa celikom.

ne bi mene iznenadilo da oni imaju negdje skrivene već izgrađene brodove, dok je železo bilo jeftino, ako Evergrande ima onolike izgrađene stanove, ma imaju sigurno i brodova, samo čekaju dobru cijenu

-

Zna li se od cega ce se raditi ovi novi brodovi, jel izmisljen neki novi materijal s obzirom da svi narucuju u Kini a problemi sa celikom.

ne bi mene iznenadilo da oni imaju negdje skrivene već izgrađene brodove, dok je železo bilo jeftino, ako Evergrande ima onolike izgrađene stanove, ma imaju sigurno i brodova, samo čekaju dobru cijenu

U pecini negdje, samo cekaju da izrone.

-

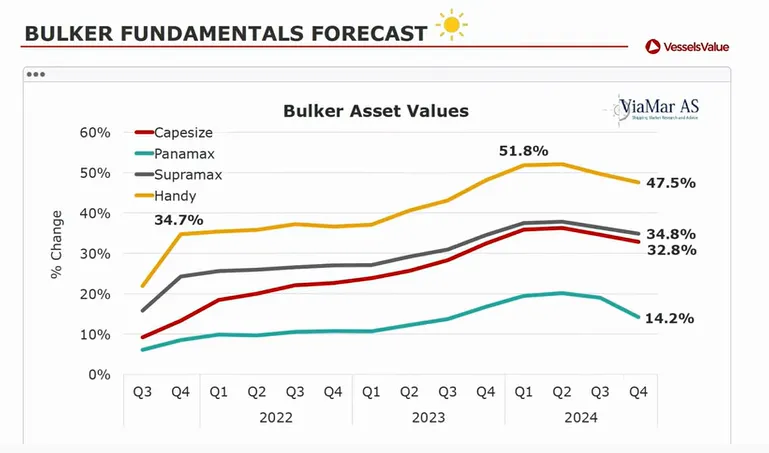

Dok se izgrade novi brodovi ipak će proći nekoliko godina a do tada će ovi postojeći puno zaraďiti.

Jednostavno je sve je se poklopilo pandemija, ogromna potražnja a brodova nedostaje.

I zato će brodarske bulk dionice otići na velike visine (bezveze je da to zovem raketom).

-

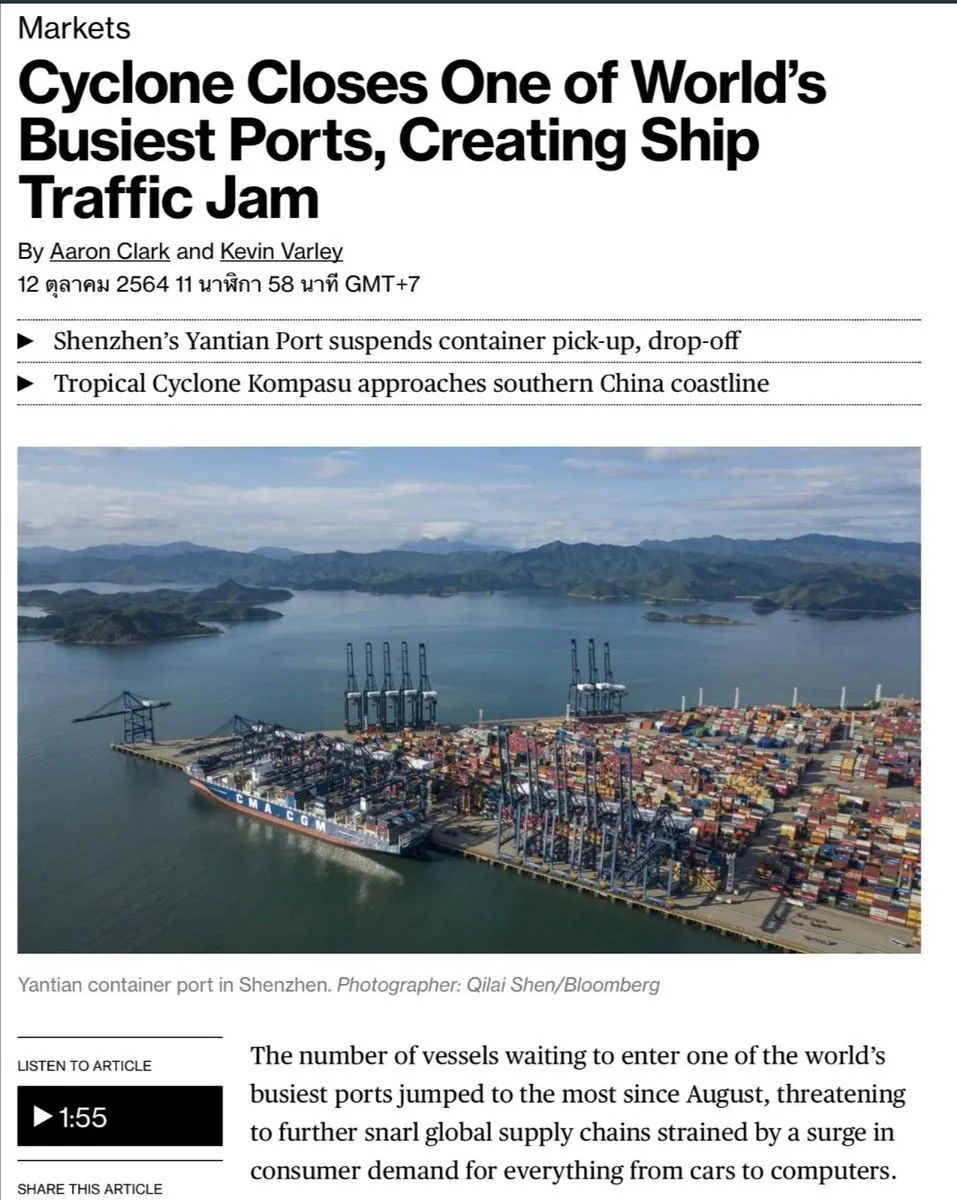

I jos malo uragana da zacini stvar, vrijeme je za brodare da se malo oporave nakon toliko godina patnje...

-

The possibility of the so-called La Nina weather pattern occurring this year has tripled, according to forecasts, potentially exacerbating an already tight global coal supply situation over the winter.

Australia’s bureau of meteorology on Tuesday forecast a 70% likelihood of the event returning over the southern hemisphere summer, which lasts from December to February.The US National Oceanic and Atmospheric Administration also forecast a 70-80% chance that the phenomenon would occur.

The event is generally associated with above-normal rainfall – often resulting in flooding – in affected areas, including key coal producers Australia and Indonesia.

But it can also lead to colder-than-average temperatures in China and other consuming nations, triggering increased demand for power generation fuels.

“This is definitely going to hurt, if La Nina shows its teeth and causes further supply disruptions in major coal-producing areas,” said a coal analyst with a European energy firm.

Strong monsoon season a concern

“Supply is already tight, so a strong monsoon season in Indonesia or Australia would take more volumes away from the market at a time when China and India are suffering due to low stocks.”

She said temperatures in northeast Asia were also forecast to be below normal, thereby lifting heating demand and proving supportive for both coal and gas prices.

Already, the Global Coal Newcastle Index – a benchmark for Pacific coal trading – last week reached a record high of USD 247.53/t.

It was last seen at USD 235/t, up more than USD 150/t from the start of the year.

Cold winter more worrisome

An Australian coal trader, however, said the potential for La Nina was not “a major consideration” at present, given the existing tightness of supply.

“I am sure it will come into the rhetoric from suppliers, as we move forward in time, but the reality is that there isn’t enough coal available today, regardless of potential future weather impacts.”

“I think there is more concern, or focus, on whether the winter will be cold in Asia and Europe, as, if it is, then there is no chance supply will be sufficient,” he said.

Pacific impact in Atlantic

The first analyst also pointed to heavy rains in Colombia and South Africa – also key coal producers – meaning the Atlantic basin market was also “not getting away with it”.

“There is no significant evidence of temperature anomalies in Europe [this winter], but the impact from the Pacific energy market will definitely end up being felt in the Atlantic,” she said.

The front-quarter API 2 contract recently changed hands up USD 9.50/t on the previous settlement, at USD 202.50/t.

-

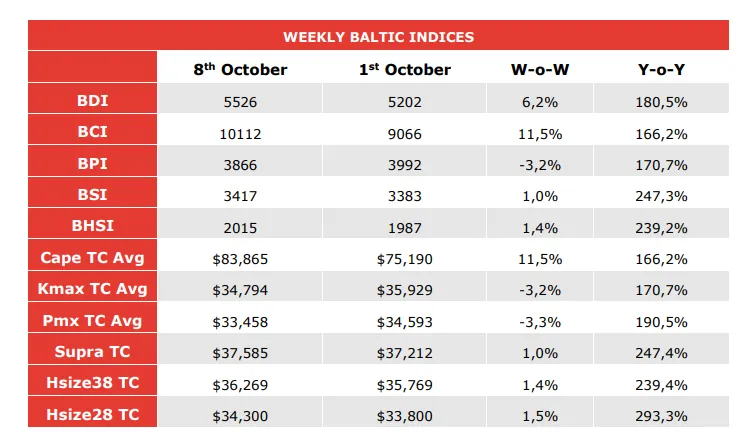

BDI 5378 (-110)

BCI 9590 (-385)

BPI 3906 (+29)

BSI 3461 (+30)

BHSI 2018 (-2)

-

-

Route Description Size Value ($) Change

BCI 5 T/C routes 180000 79535 -3187

BPI 5 T/C routes 82500 35150 257

BSI 10 T/C routes 58328 38069 325

BHSI 7 T/C routes 38200 36317 -40BDI INDEX 5378 -110

-

I jos malo uragana da zacini stvar, vrijeme je za brodare da se malo oporave nakon toliko godina patnje...

Prvo zastoj u potraznji a nakon toga luda potraznja i raketa na vozarinama.

Idemo dalje za iste pare... 😁

-

I jos malo uragana da zacini stvar, vrijeme je za brodare da se malo oporave nakon toliko godina patnje...

Prvo zastoj u potraznji a nakon toga luda potraznja i raketa na vozarinama.

Idemo dalje za iste pare... 😁

Do petka bi se trebalo smiriti vrijeme

-

Zna netko zašto Joakim predviđa toliko niže vozarine za Handye, a sada su al pari s ostalima?

Ima fetis na zimske crnjake😂

Prije 12 mj je prognozirao zimski potop.

Opet ce ga u sijecnju taj fetis popustiti.

Mora se prvo uvjeriti na svoje oci da se rjesi bugova(virusa) i opet ce biti onaj pravi stari The Joakim.

Trenutno nije svoj,sezona je pecurki🤭

Bez njega idemo dalje a on ce se pridruziti... 😁

-

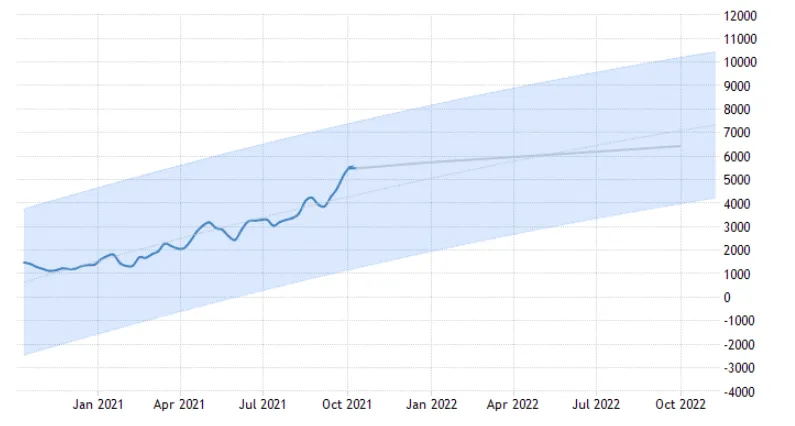

Slika govori sve.......

-

Baltic Exchange Dry Index is expected to trade at 5739.30 points by the end of this quarter, according to Trading Economics global macro models and analysts expectations. Looking forward, we estimate it to trade at 6430.05 in 12 months time.

Možeee

-

BCI 5 T/C routes 180000 79535 -3187

BPI 5 T/C routes 82500 35150 257

BSI 10 T/C routes 58328 38069 325

BHSI 7 T/C routes 38200 36317 -40

BDI INDEX 5378 -110

Pnmx i Smaxi dobar rast danas

Idemo dalje...

-

Najnovija prognoza IMF za 2021 kaze smanjen rast kineskog GDP sa 8,1 na 8,0 🤔🤭

Ne prate vijesti o zatvaranju nekih tvornica jer nema struje,o skracenom radu?

To ce biti nizi rast ne za 0,1% nego >1%.

3q ce to manje a 4q vise pokazati.

Nisu 🇨🇳Drugovi i drugarice bez razloga pokrenuli investicije u infrastrukturu jos u augustu.

-

BMTI Handy Bulk Overview (12 Sep 2021)

The chartering world remains a mixed bag of news, albeit one that continues to enrich the owners at any rate. Off the Continent, scrap charterers took a 56,000 dwt at US$ 35,000 daily to the East Med, which fixture is dwarfed by the fixture of a 35,000 dwt at US$ 36,500 to a similar destination WCSA charterers took a 58,000 dwt in the low US$ 40,000 daily for a trip via WCSA and redelivery Cristóbal. From the Black Sea, grain charterers are struggling to cover Handysize cargoes with tonnage tight and rates up. For Nikolayev to Tunisia there has been tonnage concluded at a rate of US$ 62/mt. Even for a 30,000mt grain cargo from less expensive Black Sea ports to the Egyptian Med, rates are somewhat in the US$ 50/mt range. Lau Lau managed to replace a vessel running late with a similar size vessel at US$ 60,500 daily for a trip to the East. Lucky them!

Tonnage of 35,000 dwt was proposed by owners for a trip from the East Med via Black Sea to the US Gulf at US$ 45,000 daily. And a 31,000 dwt vessel has been linked with a trip to the ECSA at a handsome freight level of US$ 37,000 daily. The Red Sea appears insanely hot, with rates for to the East with owners’ rates climbing from US$ 45,000 daily to US$ 60,000 daily within only two hours. Also, from South Africa, Handysize tonnage is being rewarded with lovely numbers like US$ 32,000 daily on a 35,000 dwt from Reunion Island via South Africa to the Continent.

Alas, a 32,000 dwt failed at US$ 45,000 daily for a trip from DES to China. OSR, the Dutch juggernaut, were said to be bidding tonnage which came in at US$ 44/mt for 55,000mt fertilizers to ARAG. From West Africa, Far Eastern log charterers seem pretty helpless in their quest for Handysize tonnage willing to go East. Owners prefer Atlantic trading. A 50,000 dwt vessel has been rumoured as done at US$ 28,000 daily for a trip from West Africa to Scandinavia. From ECSA several charterers are busy replacing vessels running late, hence higher head rate. A rate of almost US$ 40,000 daily on a 53,000 dwt with delivery West Africa via Plate to Myanmar is not to be sniffed at.

From the WCCA, grain charterers are desperately endeavoring to cover a cargo of 30,000mt grains to Algeria for which tonnage has been offered at US$ 95-100/mt. Charterers need to open their pockets. A rate of US$ 85/mt seems too low. In the East, a 32,000 dwt vessel was closely traded at US$ 40,000 daily for a trip from CIS to China. Owners of a 34,000 dwt vessel would like to have US$ 36,000 daily for 2-3 laden legs, whilst owners of a 56,000 dwt vessel were holding out for a rate of 38,000 daily for 4-6 months of trading.

-

Display More

BMTI Handy Bulk Overview (12 Sep 2021)

The chartering world remains a mixed bag of news, albeit one that continues to enrich the owners at any rate. Off the Continent, scrap charterers took a 56,000 dwt at US$ 35,000 daily to the East Med, which fixture is dwarfed by the fixture of a 35,000 dwt at US$ 36,500 to a similar destination WCSA charterers took a 58,000 dwt in the low US$ 40,000 daily for a trip via WCSA and redelivery Cristóbal. From the Black Sea, grain charterers are struggling to cover Handysize cargoes with tonnage tight and rates up. For Nikolayev to Tunisia there has been tonnage concluded at a rate of US$ 62/mt. Even for a 30,000mt grain cargo from less expensive Black Sea ports to the Egyptian Med, rates are somewhat in the US$ 50/mt range. Lau Lau managed to replace a vessel running late with a similar size vessel at US$ 60,500 daily for a trip to the East. Lucky them!

Tonnage of 35,000 dwt was proposed by owners for a trip from the East Med via Black Sea to the US Gulf at US$ 45,000 daily. And a 31,000 dwt vessel has been linked with a trip to the ECSA at a handsome freight level of US$ 37,000 daily. The Red Sea appears insanely hot, with rates for to the East with owners’ rates climbing from US$ 45,000 daily to US$ 60,000 daily within only two hours. Also, from South Africa, Handysize tonnage is being rewarded with lovely numbers like US$ 32,000 daily on a 35,000 dwt from Reunion Island via South Africa to the Continent.

Alas, a 32,000 dwt failed at US$ 45,000 daily for a trip from DES to China. OSR, the Dutch juggernaut, were said to be bidding tonnage which came in at US$ 44/mt for 55,000mt fertilizers to ARAG. From West Africa, Far Eastern log charterers seem pretty helpless in their quest for Handysize tonnage willing to go East. Owners prefer Atlantic trading. A 50,000 dwt vessel has been rumoured as done at US$ 28,000 daily for a trip from West Africa to Scandinavia. From ECSA several charterers are busy replacing vessels running late, hence higher head rate. A rate of almost US$ 40,000 daily on a 53,000 dwt with delivery West Africa via Plate to Myanmar is not to be sniffed at.

From the WCCA, grain charterers are desperately endeavoring to cover a cargo of 30,000mt grains to Algeria for which tonnage has been offered at US$ 95-100/mt. Charterers need to open their pockets. A rate of US$ 85/mt seems too low. In the East, a 32,000 dwt vessel was closely traded at US$ 40,000 daily for a trip from CIS to China. Owners of a 34,000 dwt vessel would like to have US$ 36,000 daily for 2-3 laden legs, whilst owners of a 56,000 dwt vessel were holding out for a rate of 38,000 daily for 4-6 months of trading.

Ma kakvi crnjaci na dry bulku? Joakime crni Joakime ostavi se pecurki,pusti da drugi beru a ti se primi svog posla i idemo dalje... 😁

-

-

Nepročitani postovi

-

- Title

- Odgovora

- Zadnji odgovor

-

-

-

ADPL (AD Plastik d.d.) 3.6k

- Admin

July 27, 2026 at 9:12 PM

-

- Odgovora

- 3.6k

- Pregleda

- 1.9M

3.6k

-

-

-

-

ATGR (Atlantic Grupa d.d.) 372

- harpun

July 27, 2026 at 7:44 PM

-

- Odgovora

- 372

- Pregleda

- 169k

372

-

-

-

-

DLKV (Dalekovod d.d.) 3.3k

- harpun

July 27, 2026 at 3:19 PM

-

- Odgovora

- 3.3k

- Pregleda

- 1.6M

3.3k

-

-

-

-

KODT (Končar - Distributivni i specijalni transformatori d.d.) 2.3k

- harpun

July 27, 2026 at 1:54 PM

-

- Odgovora

- 2.3k

- Pregleda

- 1.2M

2.3k

-

-

-

-

ULPL (Alpha Adriatic d.d.) 1.6k

- Manu

July 27, 2026 at 1:45 PM

-

- Odgovora

- 1.6k

- Pregleda

- 672k

1.6k

-