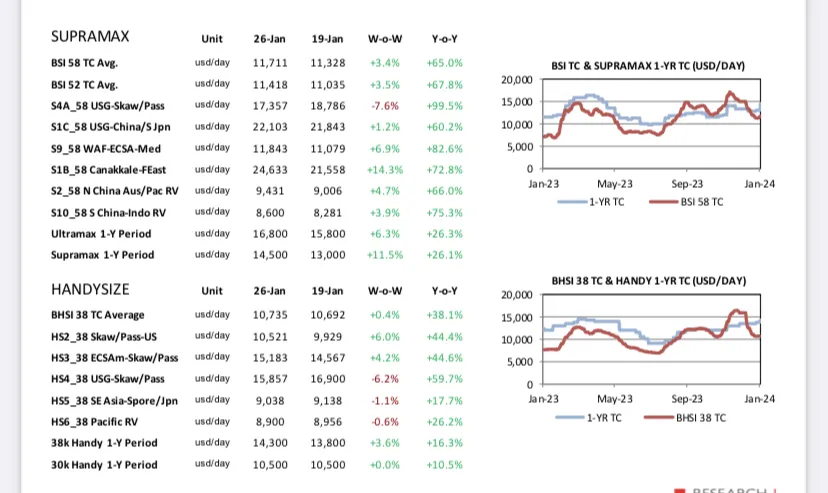

Lijepo je vidjeti zelenilo na svim rutama kud plove brodovi 🫡

Podaci iz izvješća banchero costa koga zanima više…

Lijepo je vidjeti zelenilo na svim rutama kud plove brodovi 🫡

Podaci iz izvješća banchero costa koga zanima više…

Sve zeleno a kineska nova godina za par dana...

Chinese New Year 2024 will fall on Saturday, February 10th, 2024, starting a year of the Wood Dragon. As a public holiday, Chinese people will get 8 days off from work from February 10th to February 17th in 2024.

Sve zeleno a kineska nova godina za par dana...

Chinese New Year 2024 will fall on Saturday, February 10th, 2024, starting a year of the Wood Dragon. As a public holiday, Chinese people will get 8 days off from work from February 10th to February 17th in 2024.

ne započinji molim te, nekima se još vrti od prošloga dočeka, a mali vodeni zeko umjesto da zapliva i skoči, zaronio i ne izranja

ali što jest, jest, pisalo je osim što je godina vodenoga zeke, da je i godina Nadanja, pa eto sve je točno, nadati se na burzi nije ništa neobično

Malo sam istraživao koliki bi bili troškovi novih ekoloških nameta za promet u EU lukama koji se obračunavaju od početka godine. Ti troškovi uopće neće biti zanemarivi. Preračunato na usd/dan na potrošnju jednog supramaxa npr. prema burzovnoj vrijednosti mtCO2e krajem 2023. to bi bilo oko 2500 usd po danu za 2024., za 2025. već oko 4100 usd/dan a 5800 usd/dan za 2026. s obzirom da se obračunava 40% za 2024., 70% 2025. a nakon toga 100%. Za promet između EU luka i ostatka svijeta obračunat će se pola iznosa a potrošnja CO2 iz 24. na naplatu dolazi u 25.

koliko pratim Verige vozi po pacifiku ako negrijesim dnevna vozarina tokvih tankera je 56k dolaraza mjesec im istjece ugovor

Malo nebitnih podataka BCI +5,53%

![]()

![]()

![]()

Malo nebitnih podataka BCI +5,53%

Malo dodatnih podataka BCI +10,69%

BCI 5 T/C routes 180000 19663 1897

BPI 5 T/C routes 82500 12851 83

BSI 10 T/C routes 58328 11450 39

BHSI 7 T/C routes 38200 10381 -97

BDI INDEX 1516 +80

Kineska nova godina donosi capesize spot vozarine na najvišoj razini u 15 godina

Dok je u Kini u tijeku slavlje Godine zmaja, vlasnici Capesizea imaju svoju prekretnicu za slavlje, s Capesize spot vozarinama na najvišoj razini u 15 godina za ovo doba godine, u razdoblju koje je tradicionalno označavalo najnižu točku za bilo koju godinu.

Atlantik ostaje glavni pokretač tako zapanjujuće, ali iznenađujuće izvedbe, dok razlozi koji stoje iza trenutne snage upućuju na neadekvatnu ponudu plovila na zapadnoj hemisferi. Iako statistike pokazuju trivijalan utjecaj trenutnog poremećaja u Crvenom moru kada je u pitanju suhi rasuti teret, čini se da je tonaža balasta doista dislocirana (u vrijeme kada suša Panamskog kanala utječe na ponudu brodova), što je dovelo do nedostatka plovila koji već traje mjesecima u tom dijelu svijeta.

Kombinirajući gore navedeno s općim optimizmom u svakom segmentu brodarstva, doista nije teško zamisliti spot tržište koje će ostati snažno kroz dugo vremensko razdoblje. FFA već uračunavaju takav scenarij sa vozarinama za sljedeće dvije godine iznad 20.000, što je porast koji se nije dogodio od kasnih 2000-ih za Capesize brodove.

....

Dobar pregled stanja; ima još korisnih podataka u analizi koga zanima na linku.

Ukratko, sjajan početak godine za brodare ![]()

Evo nama Capeovi neloših +17,29%na tjednoj osnovi na 2.381, na cca 19.300$

Pratimo dalje, naravno i ostale klase ❤️👍😎

Evo nama Capeovi neloših +17,29%na tjednoj osnovi na 2.381, na cca 19.300$

Pratimo dalje, naravno i ostale klase ❤️👍😎

valjalo bi to i proslaviti ![]()

Evo nama Capeovi neloših +17,29%na tjednoj osnovi na 2.381, na cca 19.300$

Pratimo dalje, naravno i ostale klase ❤️👍😎

valjalo bi to i proslaviti

Ovako su jeli pangoline prije par godina pa nije dobro ispalo. Ali ajde, ovo je samo malko neobicna kokos😎

BCI 5 T/C routes 180000 20304 454

BPI 5 T/C routes 82500 14817 210

BSI 10 T/C routes 58328 11783 143

BHSI 7 T/C routes 38200 10287 74

BDI INDEX 1610 +29

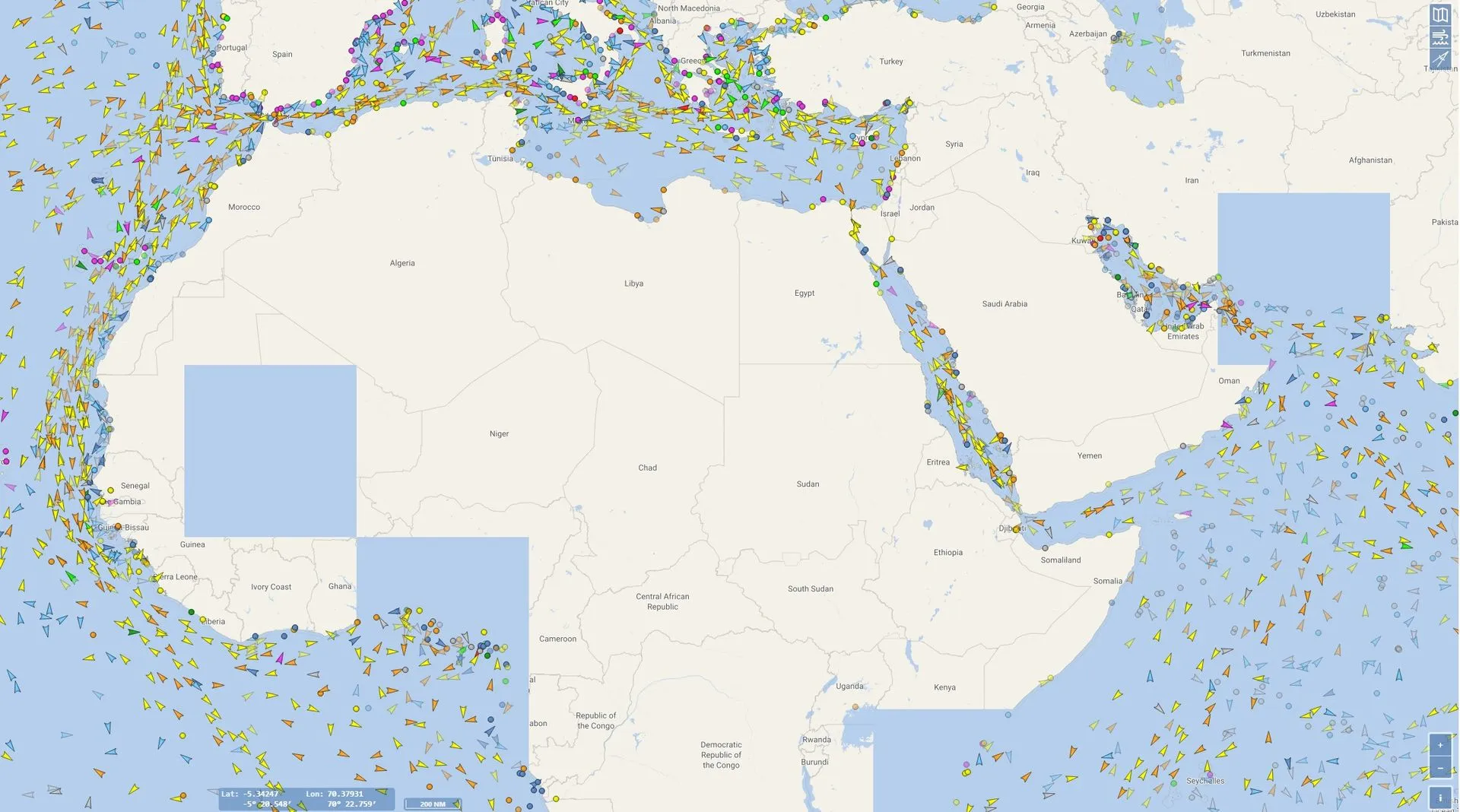

Ako koga zanima kako to izgleda kada je Sueski kanal izvan funkcije...

Ako koga zanima kako to izgleda kada je Sueski kanal izvan funkcije...

To je valjda nevečer bilo crveno...jutros je zeleno na semaforu

brodovi prolaze samo je pitanje čiji i pošto? to je još jedan evidentni udar na evropsku ekonomiju od nazovi saveznika.

Tu su sve vrste plovila. Pitanje je koliko su od toga međunarodni teretni brodovi. I dalje se plovi na rizik

On Friday, the International Bargaining Forum (IBF) – where crew employers and unions meet – revealed an agreement allowing seafarers to refuse to sail on ships passing through the Red Sea.

Ako koga zanima kako to izgleda kada je Sueski kanal izvan funkcije...

To je valjda nevečer bilo crveno...jutros je zeleno na semaforu

Ma ja sam nasao za kontejnerase, vidim da ti imas bulkere. Sa koje stranice si to stavio?

Poanta je da ih jako puno, barem kontejnerasa izbjegava Sueski kanal.

Belships REPORT 4TH QUARTER 2023 Market highlights

In the fourth quarter, the Baltic Supramax Index (BSI-58) averaged USD 14 159 per day –

significantly up from USD 10 028 per day in the preceding quarter. The Baltic Ultramax Index (BSI63) averaged USD 16 189 per day in the fourth quarter, up from USD 11 837 per day in the third

quarter. The market peaked in December when the Supramax index reached USD 17 213 per day,

which translated into almost USD 20 000 per day for Ultramax vessels.

Asset values followed suit and rose gradually in the fourth quarter. By the end of the year values

were back to about the same levels as at the start of the year. Even though long-term interest rates

rose during 2023, they receded in the fourth quarter, and we would opine that this contributed to

rising ship values. Ship values have continued to rise in 2024, especially for modern vessels which

continue to be markedly higher in demand than less economical older ships.

According to Fearnleys, preliminary estimates for Q4 2023 shipment volumes were 283 million

tonnes, an all-time high, after the previous record of 279 million tonnes in the preceding quarter.

The highest growth (quarter-on-quarter) was seen in iron ore (67 per cent), coal (9 per cent) and

steel products (10.6 per cent). Minor bulks (-11 per cent), grains (-7 per cent) and fertilizers (-3 per

cent) contributed negatively. We continue to observe a variation in growth figures of each

commodity type from one quarter to another, however, total shipment volumes were up 1.2 per

cent quarter on quarter, and total demand appeared robust throughout 2023.

Port congestion, as measured by the average waiting time in port for ships to discharge, continued

at close to the same levels as in the third quarter. However, waiting time in port for ships to load

increased somewhat due to delays in South America caused by low inland water levels. Reduced

capacity in the Panama Canal also reduced efficiency, causing longer sailing distances for vessel

operating in and out of the Atlantic Ocean. This effect has continued into 2024, and further

inefficiencies are added from vessels avoiding transits through the Red Sea and the Suez Canal. As

we have highlighted before, changes in port congestion, voyage duration and/or vessel speeds

affect the overall vessel efficiency in the dry bulk market on a short-term basis more than a change

in the number of newbuildings in the orderbook.

33 Supra/Ultramax vessels were delivered in Q4 2023, compared to 32 vessels in the previous

quarter, according to Fearnleys. At the time of writing this report, 16 new vessels have been

delivered in 2024, with about 160 scheduled for delivery this year. However, actual deliveries are

likely to be slightly lower due to slippage or cancellations. Fleet growth has been around 3.5 per

cent since May 2023. According to Fearnleys, this rate of fleet growth will be maintained through

2024. The number of ships delivered per quarter compares to an existing fleet of Supra/Ultramax

vessels on the water today of about 4 100 in total. The orderbook for dry bulk remains close to alltime lows at about 8 per cent.

Relatively low newbuilding activity for dry bulk continues as the lack of conviction and alternatives

for fuel and propulsion systems appear to restrain new orders. Higher input costs as well as full

orderbooks and continued high demand for other vessel segments dictate the position with

shipyards.

Available delivery positions with reputable shipyards appear increasingly distant, with some new

orders being reported in 2027, and even 2028. A potential lead time of four years for a bulk carrier is

unprecedented. Belships ASA - quarter report (globenewswire.com)

Drybulk FFA (derivatives)positive today. Cape FFA flat on front, up in Q2->Q4. Pmx and Smx FFA moving up.

![]()

![]()

![]()

![]()

![]()