Samo da Capex ne povuce za sobom dolje i ostale klase...i to za vrijeme OI...

Samo neka ne bude produžetaka na OI i neka se sve završi na vrijeme.

Samo da Capex ne povuce za sobom dolje i ostale klase...i to za vrijeme OI...

Samo neka ne bude produžetaka na OI i neka se sve završi na vrijeme.

Rezultati 2020 bulkers, q4

Imaju i očekivanja za 2022. godinu i pregršt podataka. Ovo je ujedno prilika i za stručnjake da istaknu da 2020 imaju capeove.

Dobro je, danas je sve normalno, bdi raste, brodari padaju. Kad je obratno, onda ne valja. ![]()

Ma Rusi će prošetat kroz Ukrajinu, to bude rat od 45 minuta. Ovo je više vapaj prema FED-u da ne dira ništa. ![]()

ZIM je nedavno imao ATH, možda i početkom tjedna. Bilo je i logično da se malo hladi, a kamoli neće u ovakvim petcima. Uostalom, imaš i jednostavno objašnjenje, hipotetski - Gle, Netflix je pao 25% u jednom danu, malo je to pretjerano, ZIM mi je odradio ne znam, 20% u tjedan dana, ajde da se malo prebacim u Netflix, ćopim neki odbijanac i to. Kao što rekoh, meni je nesigurno biti izvan ZIM-a pa to ne radim, ali ima ih koji rade.

Stvarno mislite da neko pretace iz zima u netfliks?

Neznam, meni je ova korekcija sve manje stealth, bas se dobro vidi na radaru

Naravno da postoje. Uostalom, što biste vi radije radili, gledali uzbudljiv triler na Netflixu ili se smrzavali na kontejnerašu koji pritom nije ni vaš nego je u čarteru. Može ZIM padati dokle hoće, ali kad izađu q4 ili objave neku vijest, prisjete se ulagači za čas zašto ga vole.

Display More

Bilo je i vrijeme da se neke dione ispušu. Valuacije su u nebu već odavno, konačno izgleda da se "bubble" na tim dionama ispuhuje. Hrpa je diona koje su otišle u nebo a ne zarađuju ništa ili nešto malo samo zbog "vjere" da budu u budućnosti. Ja navijam da se taj pad nastavi sve dok ne budemo više na zemlji sa valuacijama.

Sve 5 kolega ali ne ispuhuje se samo prenapuhano nego sve redom. Ja imam samo niske p/e i to value dionice a jucer me dobro nagazilo. Ne mogu biti dalje nego jesam od nekih netfliksa i pelotona pa opet krv.

U ratu bi ovo nazvali neselektivno granatiranje

P.S. ovaj je to lijepo sazeo:

https://www.cnbc.com/2022/01/20/sto…close-news.html

“Until a level is reached in this collapse... fundamentals like bond yields, economic reports and even earnings releases will not likely have much impact. Fear now must be extinguished by some stock market stability before traders and investors again start to consider fundamental drivers,”

ZIM je nedavno imao ATH, možda i početkom tjedna. Bilo je i logično da se malo hladi, a kamoli neće u ovakvim petcima. Uostalom, imaš i jednostavno objašnjenje, hipotetski - Gle, Netflix je pao 25% u jednom danu, malo je to pretjerano, ZIM mi je odradio ne znam, 20% u tjedan dana, ajde da se malo prebacim u Netflix, ćopim neki odbijanac i to. Kao što rekoh, meni je nesigurno biti izvan ZIM-a pa to ne radim, ali ima ih koji rade.

Evo još jednog zanimljivog webinara Capital Linka

Zadnjih mjesec dana osim nafte opet brutalno poskupljuje sva metalurgija. Stvarno ružno izgleda koliko to ide gore. Posebno bazni metali. Ne toliko srebro i zlato. A što se tiče eksplozije brodara i dalje rastu kontejneraši.

Da, cash masine i dalje gaze, danas, tj od jucer u ah posebno MATX:

Nije ni cudo:

Mintzmyer je najavio prije tjedan-dva da će se MATX vjerojatno ovih dana javiti s revizijom rezultata i buybackom, frajer prati sektor brutalno. Čak sam razmišljao prodati ZIM da uzmem MATX, ali ne mogu. Jednostavno se presigurno osjećam u ZIM-u.

Indonezia ukinula zabrane za preko 130 ćumurlija koji su ispunili svoje obveze, zato su futuresi pozelenili od muke.

OVdje je razgovor s Garyem Vogelom, CEO-om Egle bulka koji ima najsličniju flotu ATPL, taj intervju bi trebao biti za domaću zadaću svakom tko ulaže u dry bulk, a nije sklon Božjoj ruci.

11.01.2022.

Gary, again, welcome. Thanks for joining us. I want to start off with the current market balance for midsize drybulk. We had a really good year in 2021. Surprisingly, not a lot of volatility. But we did see those rates pull back a lot into this winter. What's the current situation on midsize drybulk?

GV: Yes, so I mean, you hit the nail on the head. I mean, obviously rates have pulled back from their highs, but we're finding ourselves here in mid-January with rates over $20,000 around 21,500 this morning. And while it's been a bit volatile by our by our standards, the midsize segment is far less volatile than the larger sizes. And we're coming into this year, a lot different than last year, right? Last year, we started with the Index around 11,000. And it grew from there. Whereas here we're coming in from a higher level.

So to use a sailing term, we've got a lot of boat speed here. And the balance feels really good. The order book is at historic lows. And we can talk a little bit more about that. And overall demand is really being led by the midsize, which we saw last year as well. So we feel really good as we're starting to engage into 2022.

JM: Yeah, hopefully 2022 will bring a lot of strength. Obviously, right now we're in the seasonal low point of the market, every January and February, as far back as I can remember, has not been too favorable for drybulk. There's been a lot of chatter, a lot of focus on China. There's been issues, with property sector with Evergrande, the environmental rules, they had an energy crisis, which required them to shut down some imports earlier this year. Do you see China as a major headwind in 2022? Or do you think they're going to be able to normalize a little bit more?

GV: Yeah, I mean we don't see it as a headwind. I mean, expectations for growth in China is in excess of 5% wherever you look. So I don't -- can't tell you exactly where the ebbs and flows will be. And there's always going to be surprises. But overall, it's clearly a driver. And we think there's certain growth areas, particularly coarse grains, wheat corn, very robust, soybeans continue as well.

Having said that, China is of course, a really important part overall for drybulk, but China is about 47% of major bulk demand, and only about 22% of minor bulk demand. I keep getting back to this because Eagle derives about two-thirds of its cargo base, from the minor bulk. And so we have much more diversity in terms of the commodities we carry, in terms of the geographic spread and the demand, as I mentioned, from China.

So it's absolutely important, but we have less reliance. That's also what leads to that less volatility, right. We have more areas to turn to. There might be 15, 20 different things you do with a midsize ship that comes open in China versus a capesize vessel, which is, really limited to effectively going Australia or back to Brazil.

JM: Yeah, certainly factors we need to watch. It just seems like China's impact on the drybulk market was really to sort of slam the brakes on rates in terms of October, November, December, maybe not deliberately. That wasn't their intention, but the policy changes they did certainly seemed to have that that impact. Are there any other key factors, both positive and negative that you're looking at in 2022? I guess both potential upsides, but also potentials to have more of a weaker year?

GV: Look, I mean, COVID, clearly, I think we all would have expected 12 months ago to be in a much different place today. So no one really has, a fair, a better idea of what that's going to look like. And that's a concern. And to be honest, it's a constant challenge in terms of navigating, excuse me -- navigating, in terms of port restrictions and ports being closed down, and infections and quarantines and things like that. So that's something operationally that we and everyone else, is facing and crew repatriation continues to be a challenge.

In terms of, demand, as I mentioned, expectation going forward is that minor bulk demand will really lead drybulk demand next year, by 2.3%, which is a fairly muted number, but seen against fleet supply, actually looks really good. So we think that while they'll definitely will be surprises, we think that the minor bulks will continue to lead. And we've been the beneficiary as well, of what we call the spillover cargoes, right from the container sector, bagged cargoes. And we continue to see those. And obviously, container rates continue to be to be robust. So we think we're benefiting from that as well, and will continue to do so at least for the foreseeable future.

...

... obrisan dio koji se odnosi isključivo na EGLE, a ne toliko na dry bulk, obrisano da stane u 10.000 znakova za post

...

So we feel good about that. To go out and buy more ships at today's levels, we would need to see a compelling reason, in terms of the forward curve. At the moment, the forward curve is backwardated, even into 2023, which, frankly, I find -- I understand it, but I think the fundamentals would point to a stronger relationship of the end of 2022 and 2023, given the order book, given COVID, and there is a progression going forward, not to mention EEXI.

So I'm not saying we won't acquire more ships, but we're not out there actively looking to acquire one to three ships. We think we've done the heavy lifting, and we think our fleet with 53 ships is a good size for us.

...

JM: That's an internal debate. All right, Gary. Well, thanks for joining us today. I think it was useful. And we'll continue to watch the midsize dry bulk markets closely. We're hoping for -- obviously, February, March is always the seasonal trough, but we're looking for some strength, hopefully soon. And with that said, Gary, I do want to give you the chance to close on -- look, there's a dozen drybulk firms out there. Why should investors consider Eagle Bulk today, and what differentiates you from those peers that are out there?

GV: Yeah. Well, thanks for the opportunity. And in terms of wrapping it up, I really, really like drybulk where we are today. This is my 34th year in the industry and I think the future supply the order book looks great. And as much as drybulk looks great, the midsize even better. We have the lowest order book, compared to the drybulk fleet overall. We expect demand to continue to be led by midsize, by the minor bulks.

If you look at the forward curve, the cape market on the forward curve, when we traded a $1,500 premium for 2022 compared to the supramax, which those assets cost 1.7 times more. So we think the yield, and we talked about that in our Investor Day, you can see on our website, the yield on midsize ships has been significantly greater over 2021. And we think that'll only accelerate this year. And that's not even including the standard deviation and the impact of volatility.

We think our business model has shown we have an ability to help perform. I talked about dynamic hedging, chartering-in vessels. You mentioned the scrubber exposure right, which is -- we have 90% of our fleet exposed to widening yields, strong governance and probably the most important we have a really strong -- I think, a strong track record that we're proud of. So those are the reasons why I think Eagle is a differentiated company and love the opportunity to talk to you today about it and happy to speak to investors as well. So thank you.

JM: Thank you, Gary. And we will look forward to keeping in touch in 2022 and fingers crossed for another solid year like we had last year. And thanks again Gary really appreciate you.

GV: Thank you J, me too. Have a good one.

JM: You as well. This includes another iteration of Value Investor's Edge live. We just hosted Eagle Bulk, CEO Gary Vogel. Eagle Bulk trades in the U.S. market, stock symbol EGLE. I currently have a long position. As a reminder, nothing on the call today constitutes investment advice or company guidance in any form. If you're listening to this recording at a later date, please be advised that positions may have been updated.

Disclosure: I/we have a beneficial long position in the shares of EGLE either through stock ownership, options, or other derivatives.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

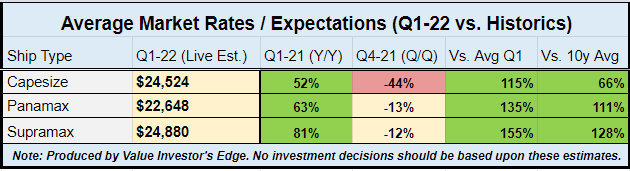

q4/21 očekivanja sa Seeking Alpha/Value Investor's Edge:

Dry Bulk Market Review

After a decade-long downturn, the bulker market showed remarkable strength during 2021, with rates setting 10+ year-highs and asset valuations regaining lost ground on the back of firming time charter rates. Strong growth in demand, coupled with port congestion and cascading effects from strength in the containership market have created a supply-demand imbalance from which the overall market has profited.

Although spot rates have declined as of late, this is fully expected due to the seasonality in the overall bulker market, with this year’s impacts further exacerbated by the upcoming Winter Olympics set to take place in China (concretely in Beijing and Habei), which have led the Chinese government to constrain economic activity to reduce air pollution levels.

Additionally, China continues to apply its zero COVID policy, which has led to substantial trade disruption throughout 2021 and into early-2022. For instance, extremely strict measures will be applied during the Olympics (“local support workers, including volunteers, cooks and drivers, are also part of a sealed bubble. They’ll have no physical contact with the outside world, even with their families”), exceeding the strict requirements which were applied in Tokyo during last summer’s Olympics.

China, as the world’s largest importer of raw materials, is the primary driver for either strength or weakness in the bulker sector, and even though the country’s economy performed exceptionally well during 2020 on a relative basis given the coronavirus pandemic, 2021 had both its ups and downs. For instance, iron ore imports eased 4.3% on a y/y basis from 2020, which had marked a record annual high. Iron ore imports have been under further pressure due to mandated curbs on steel production. During the first five months of 2021, imports were very strong, up on a y/y basis, but during H2, “authorities urged steel mills to cut production to meet an annual target of keeping crude steel output flat” (link), which weighed heavily on annual import levels.

The billion-dollar question is whether iron ore imports will regain part of their lost ground during 2022. Economic activity in China seems to be under pressure, given not only turmoil in the property sector, but also in retail, with Nike sales in Greater China down 13% on a constant currency basis for the six months ended November 30th versus the same period a year earlier (link to Nike’s Q3 report). Starbucks also reported lower sales in China, with comparable store sales down 7% on a y/y for Q4, due to a 5% decline in average ticket and a 2% decline in transactions (link), albeit that includes “adverse impacts of approximately 4% from lapping prior-year value-added tax exemptions”.

These concerns were validated when China’s central bank cut its main interest rate by 5 basis points to 3.8%, the first cut in 20 months. Part of the weakness in the overall economy is attributable to pandemic-induced curbs under the prevailing zero COVID policy, but the real estate sector has also made headlines in negative fashion. Additionally, the Chinese central bank lowered the reserve requirement ratio “for most banks by half a percentage point”. During prior downturns (or decelerations), Chinese policymakers resorted to significant infrastructure spending, but it remains to be seen whether they will follow the same strategy this time around. Overall, China poses a significant risk for dry bulk markets, but it is still too early to tell whether this will translate into lower import levels during 2022.

Per Clarkson’s estimates, ton-mile demand grew around 4.8% during 2021, and is expected to grow a further 2.2% in 2022, outpacing supply additions of an estimated 3.6% and 1.6% in 2021 and 2022 respectively. Growth estimates for 2021 have been revised upwards since last quarter, but 2022 estimates have seen a slight reduction of 10 basis points. Ton-mile demand has significantly outpaced gains in overall dry bulk trade volumes, which grew 4% in 2021, and are projected to grow a further 1.6% in 2022. 2021 volumes were 2.3% higher than those of 2019, with iron ore, grain, coal, and minor bulks all seeing substantial gains on a y/y basis (albeit coal volumes remain 4% below 2019 levels). Clarkson’s expects most of the growth in 2022 will come from minor bulks and grain, whereas iron ore “is likely to see only limited growth as Chinese imports continue to “normalize” after a record 2020/1H21”.

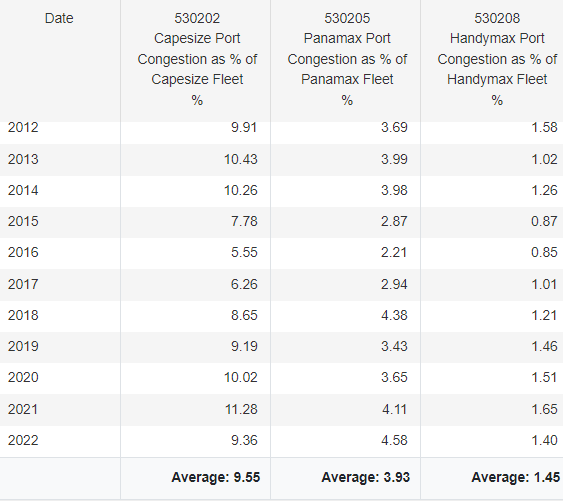

Those numbers by themselves would make for a very bullish stance considering the rates we have seen throughout 2021, since the supply/demand balance would imply further tightening during 2022, but there is another very relevant variable in the picture: port congestion. Per Clarkson’s estimates, port congestion is tying up 3%-4% of the global fleet compared with pre-pandemic levels. As can be seen in the image below, incremental congestion during 2021 was mostly centered in the Capesize class (relative to historical averages).

Source: Capesize, Panamax, and Handymax port congestion as a % of the fleet, Clarkson’s SIN.

Keep in mind port congestion in the bulker sector is very different from what we see in the containership segment (which is attributable to numerous factors in addition to COVID-induced restrictions), so it is difficult to assess whether dry bulk congestion will remain elevated during 2022. However, as long as China keeps its zero COVID policy intact, we expect to continue to see elevated congestion throughout 2022.

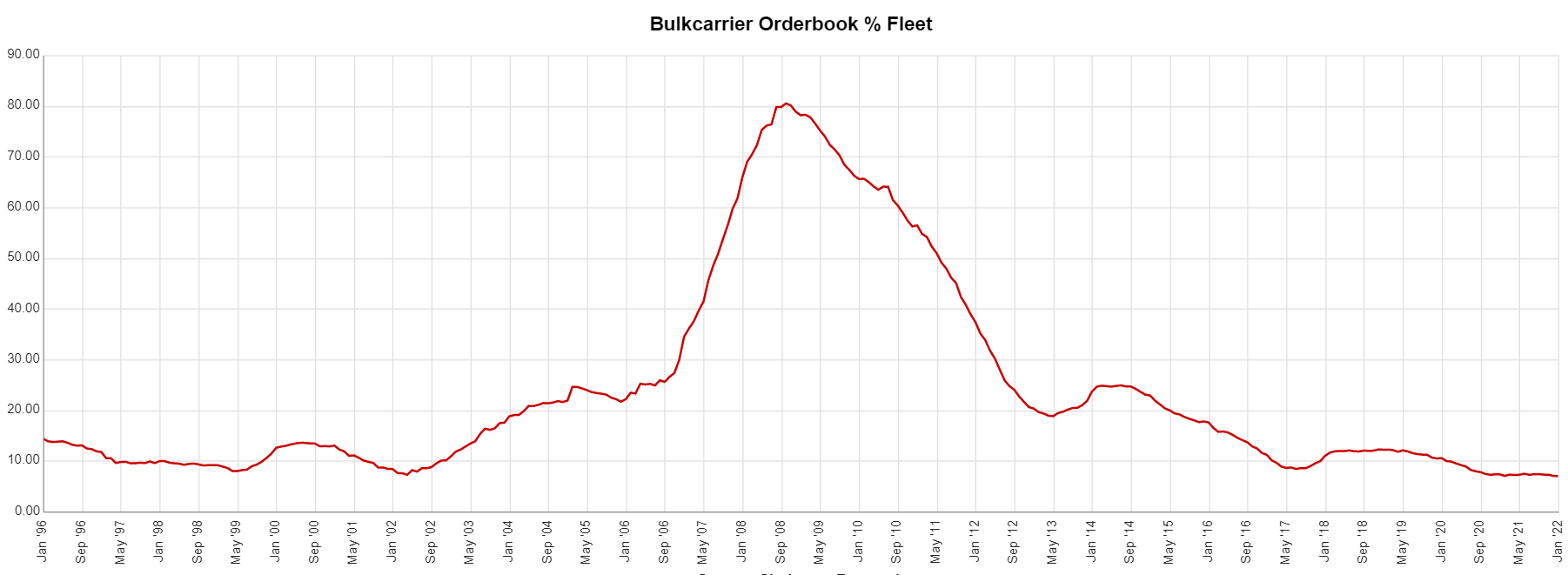

The orderbook remains extremely attractive, even after a very strong 2021, with the overall orderbook sitting at a very manageable 6.99% of the fleet, the lowest level in modern history (at least since Clarkson’s began collecting the data in 1996).

Source: Clarkson’s Shipping Intelligence Network.

Ordering slightly picked up during 2021, with 81 Capesize orders placed (100,000+ dwt), followed by 150 Panamax/Kamsarmax orders (70,000-99,999dwt), 123 orders in the 40,000-69,999 segment (Ultramaxes, Supramaxes, and Handymaxes), and 93 Handysize orders. These are all significantly higher than the number of orders placed during 2020, but ordering has been slowing as of late, with only 8, 14, 32, and 17 orders placed in the Capesize, Panamax/Kamsarmax, Ultramax/Supramax/Handymax, and Handysize segments respectively during 2H-21.

The impact from upcoming regulations, coupled with strong steel prices and yard scarcity have put a lid on ordering, and we believe orders will continue to remain scarce during 2022. Keep in mind that bulkers are the cheapest vessels to build on a nominal basis, and thus, investments in LNG dual-fuel retrofits (or other technologies) have a higher cost relative to the purchase price, since they can represent over 20% of the total order price (considering an LNG dual-fuel retrofit costs around $10M).

Scrapping was very low during 2021, with only 14 Capesizes, nine Panamaxes, 14 Handymaxes, and 20 Handysizes sold for scrap last year, and virtually no demolitions during 2H-21. If the market weakens, we expect to see a very decent amount of scrapping given the aging bulker fleet, especially if scrap steel prices remain at very attractive levels. Overall, the bulker market has a very attractive supply side, but concerns regarding the Chinese economy have clearly made a dent on overall market sentiment. China’s actions can singlehandedly change the outlook for the dry bulk market, and how they react to the recent deceleration in their economy (with infrastructure spending or not) will dictate a significant portion of dry bulk’s performance over 2022-2024.

A potential energy crunch made the headlines during late-Q3 and early-Q4, but it seems the worst possible scenarios have so far been avoided. Indonesia announced a coal export ban until it replenished inventories, but they have already relaxed their stance, allowing for the departure of 37 vessels. Overall, energy pricing (LNG, coal, crude, etc.) remains strong, but so far supply has kept up with demand. Going forward, investors will need to continue to monitor developments in China to best assess the future of the bulker market. At least until after the Chinese New Year and Winter Olympics, we expect rates will remain under pressure.

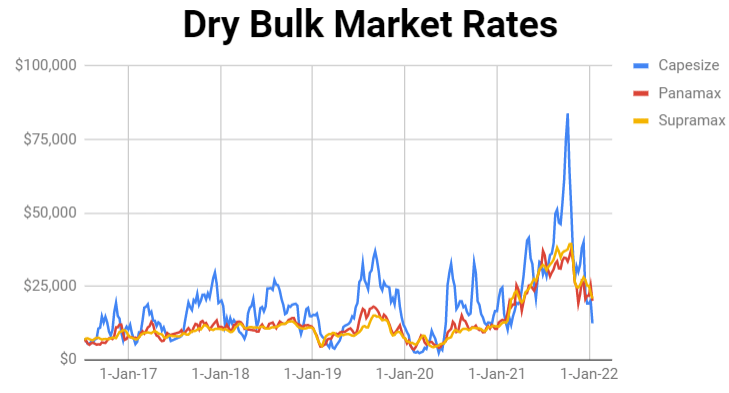

The chart below shows the past few years of dry bulk rates. As can be seen, the dry bulk market is very seasonal with rates typically much stronger in the second half of the year versus lower rates in the first half. We can also see the brief October spike in rates, followed by seasonal weakness as we approach Chinese New Year.

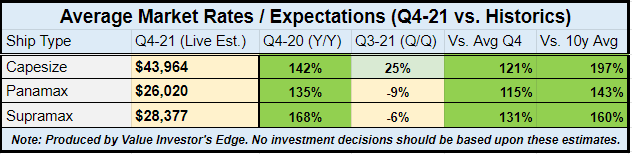

Q4 averages have been exceptionally strong on a y/y basis, albeit mixed on a q/q basis, with Capsizes gaining 25%, but Panamax and Supramax rates down 9% and 6% respectively. These rates are also exceptionally strong when compared against historical averages, with rates up between 115% and 131% when compared with historical Q4 averages.

We are at the very early innings of Q1-22, but on a q/q basis, the trend is clearly to the downside, which is unsurprising given the seasonality in the bulker sector. However, on a y/y basis, as well as compared with historical averages, rates are still at very strong levels (even though we expect Q1 averages to come in well below current levels, especially for Capesizes).

Slušao sam jučer intervju s menagementom Starbulka. Oni govore da nije toliko problem (ili kako kažu Kinezi izazov) sa EEXI koliko sa CII. EEXI je jednokratno ulaganje, ali CII koji će se mjeriti od 2023. godine je proces koji se mjeri tijekom cijele godine i svake godine. Ona kažu još i da se novi brodovi u dry bulku ne naručuju zato što bi se trebali naručivati s horizontom do 2030. godine, a nitko ne zna koje će se gorivo tada upotrebljavati. Kaže, lako kontejnerima, njihov horizont nije toliko dugačak, oni će brodove otplatiti za 5 godina pa im je sad svejedno.

Onda još vele da ako danas naručiš novi brod, nema šanse da ti bude isporučen prije 2024. godine. Jako dobar intervju sve u svemu, okačit ću ga ovdje kad transkript bude dostupan, inače ga je vodio J. Mintzmyer.

Iduci tjedan ide izvjestaj za q4. Kakve su prognoze?

Prognoza je da ne ide izvješće za q4 sljedeći tjedan. ![]()

Je li se to kolega lagano sprema za ulaz, kada takne dno?

Buy low, sell high, to je "name of the game". Opet cu kupiti kada bude vrijeme - sada, po mom skromnom misljenju, to jos uvijek nije.

U svakom slucaju je sigurno puno lakse ove minuse gledati dok si u kesu, umjesto u dionici.

Ljudi koji ne mogu podnijeti pad obično ne mogu podnijeti ni rast.

Evo Clarksonovih prognoza za 2022. godinu

Imam, s Twittera je, vjerojatno se plaća da se vide svi detalji:

Evo malo o lanjskoj Božjoj ruci:

1) 2021 was the most productive year to date for the Dry Bulk sector. In the past 12 months, 16K+ active #vessels of all sizes carried out 150K+ #voyages, transporting over 5.2bn MT of Dry Bulk in the process. This is a 5.2% YoY increase, adding over 257m MT to the market.

2) Nearly all major #commodities contributed to the sector growing, with #Soybeans and #Bauxite being among the exceptions, registering YoY decreases. Steam Coal saw 5.3% increase, Coking Coal - 7.1% increase, while #Steel products (including Scarps) – 15.5% increase YoY.

3) With the exception of #Supramaxes, every other vessel segment saw YoY growth in 2021. #Ultramaxes (up 10.9% YoY), #Panamaxes (up 9% YoY), Minicapes (up 16.7% YoY), and #Capesizes (up 6% YoY) set all-time highs both for voyages carried out, as well as #cargo transported.

Izvor: https://public.axsmarine.com/tradeflows?utm…mpaign=analysis

Umjesto da hitno dižu kamate oni će lajati na Mjesec do ožujka.

Znači, panična reakcija dizanja kamatnih stopa na dan kad je najviša inflacija umirila bi tržište i poslala poruku da je sve u redu?

Bilo je nekog govora ovih dana da je prošle godine zabilježen snažan rast minor bulka od 13,3% što je, među ostalim, posljedica divljanja kontejnera. Spominjalo se i ovdje da roba koja se obično prevozi kontejnerima, sve više ide u break bulk. Neki analitičar je rekao i kako su prije capeovi određivali cijenu manjih panamaxa i supri, pa recimo, ako je cape bio 90k, ovi su bili 40-30, a da je sad zbog break bulka situacija obratna pa manji brodovi određuju cijenu većih. Što se i vidi. S obzirom da nema naznaka da bi se congestion na kontejnerskim terminalima trebao smanjiti u neko dogledno vrijeme, a time i vozarine za kontejnere pasti, dry bulk bi trebao osjećati prelijevanje s kontejnera još neko vrijeme.

Sve one ostale stvari poput nikad manjeg postotka novog brodovlja i zauzetosti brodogradilišta i ekoloških standarda od 2023. itd. i dalje stoje. S tim da mrtva sezona za dry bulk obično prestaje sredinom ožujka.

Ne pratim PTKM već dugo, ali ako sama najava povlačenja s burze izaziva pad cijene, što je logično, onda je u konačnici i nebitno hoće li dionica ostati na burzi ili ne, a ko u međuvremenu cijena dionice padne i skine tromjesečni prosjek po kojem će Turci, ako kupe PTKM, biti obavezni isplatiti male dioničare. Turci ako kupe, sretno im sa sindikatima, a sretno i sindikatima s Turcima.